Hey there! This post contains affiliate links. Using my links means I earn a commission, which helps me create more rad content. More on affiliates here.

Are you trying to figure out how to improve your credit score? Well then, you’re in the right place!!

Hello! Hi! I am writing this blog post in the hopes that it makes its way to other people who feel overwhelmed by personal finance, managing their money, credit scores, and and and – all that jazz.

Opening up to the internet about some massive idiotic mistakes you’ve made. as an adult, is, well, a little intimidating. But, I’m doing it!!

Below, I’ve shared my story, as well as some key things I’ve learned about gaming (yes, gaming) your way to a higher credit score.

How to improve your credit score

Note: I originally shared this experience on my Instagram Story, as part of my #MakingMovesWithBri series on all things adulting. The goal of this series is to delve into topics that it feels like *everyone else* knows about – but we don’t!! If you’re looking. to level up in your life, be sure to check out my online courses.

My History of Credit Score Mistakes

So, I’ve had a history of making poor choices with regards to my credit. And I have to take 110% of the blame, because I grew up in a house with Suze Orman, and I had to take a financial literacy class in high school.

*Face Palm*

Timeline of My Credit Score Mistakes

Here’s a timeline with you of my credit score screw ups, so you’ll know that you aren’t alone:

- 2009: A cute girl at the mall convinced me to sign up for a credit card for one of my FAVORITE stores, a few months after I turned 18. For a purchase that was around $50, I ended up forking over something like $700 with fees (it went to collections) when all was said and done.

- 2011: I took time off from college, and turns out you have to pay on your student loans when you do this! I didn’t! One ended up going to collections.

- 2016 – Late 2018: HAD I LEARNED MY CREDIT LESSON YET? NOPE! I had a few medical bills and a credit card from a popular electronics store go to collections. Not because I didn’t have money. BUT BECAUSE I WAS TOO ANXIOUS TO OPEN THE DAMN ENVELOPES. -_-

Aside: My Money Anxiety

Did you read that last line? Picture me screeching it. I did’t make payments because, wait for it, “I WAS TOO ANXIOUS TO OPEN THE DAMN ENVELOPES.”

I shared this on my Instagram Story, and I felt like a Total and Complete Idiot. Then messages started pouring in, from readers who shared that they had also felt “immobilized” or “like a deer in the headlights” with this stuff.

We’re not alone! You’re not alone in your anxiety around money, either. And it was my lovely readers, sharing their stories, that made me decide to write about this journey.

Oh, Crap. My Credit Score Sucks

So after these various debacles, as well as making late payments on different things due to lack of organization, I realized last year (early 2019), that I really need to get my crap together.

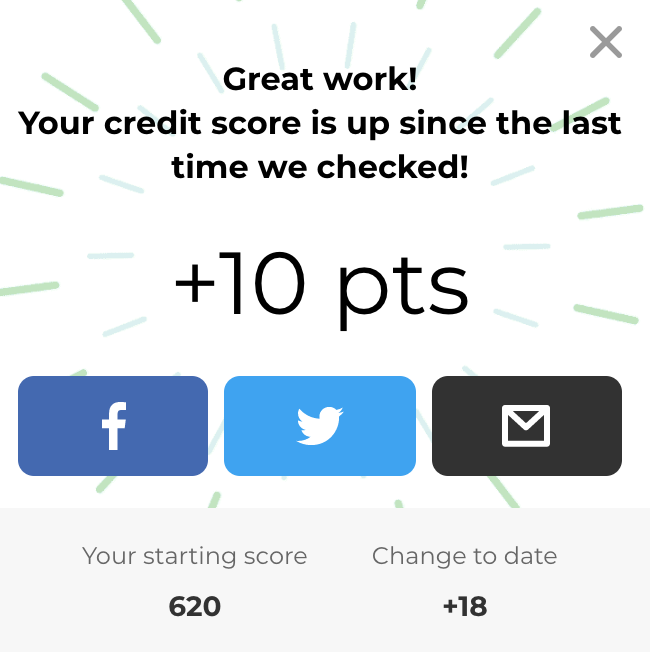

“I need to GET IT TOGETHER!!” I proclaimed to myself. I got my credit report, and the number I got back was not…. cute.

I can’t remember the exact number (did I erase it from my memory out of shame? Probs), but I know it was in the low 500’s.

My credit score is in the low 500’s

Taking My Head Out of My Butt – er, the Sand!

After seeing my craptastic credit score, I realized I could continue to bury my head in the sand. Or I could buck up, square my shoulders and begin the painful process of Dealing with My Money.

I started listening to podcasts and books (shoutout to Audible) on finance. Everything from finding a Roth IRA with advice from Suze Orman, to following finance people on Twitter to podcasts to self-help books.

I had always thought that financial education would just…. show up? Like people in my friend group would bring up their investing strategy, or I’d magically watch a Netflix docuseries and learn everything about money.

Nope.

Harsh Truth Moment: Staying in Overwhelm is a CHOICE

Something I’ve noticed, as I’ve started talking more about personal finance and getting my you-know-what together is the excuses folks share. (Why they need my approval, I don’t know!)

I hear things like:

- “Ugh, that’s just too complicated.”

- “People who worry about that stuff are shallow.”

- “I don’t worry about all that financial stuff”

- “That’s way too overwhelming!!!!!”

The System is Out to Get You (Kind Of)!!

I wish I had read this earlier in life:

Here’s the thing. Your bank, your credit card, your financial platforms – THEY DO NOT CARE IF YOU DON’T UNDERSTAND THIS STUFF. MOST INSTITUTIONS WILL PROFIT OFF OF YOUR LACK OF KNOWLEDGE.

You will continue to be kicked in the teeth, money-wise, until you square your shoulders, grit your teeth, AND START LEARNING A BOUT MONEY.

I had this ^^ painful realization, when I had a “Ohhh, no duh” moment about my credit score. *** I *** am the only person who is solely responsible for this. I can take a learned victim mentality, and complain about “The Man” and have a crappy APR % on my car and shell out money in more interest, etc, or I can buck up and LEARN.

WE ARE ALL CAPABLE OF LEARNING! DON’T SELL YOURSELF SHORT!

Where to Start – This BOOK!

If you’re super overwhelmed, I recommend starting with the book, “I Will Teach You to Be Rich.” I get my personal development via audible, so I can listen while cleaning or driving. It has a rather cheesy title, but the knowledge is SOUND.

You can get the book here!

Okay, now back to our conversation on fixing one’s credit score:

What No One Tells You: Your Credit Score is a MF GAME!!!!

As I started to learn more about building my credit, how investing works, etc etc, I came to a stunning realization:

BUILDING YOUR CREDIT IS A GAME! WITH KIND OF ARBITRARY RULES! There is some reasoning to it, but the system was just kind of… created, and it prioritizes different behaviors over others.

The credit score system feels arbitrary, because, well, it kind of is. So we have to STRATEGIZE and use TACTICS to raise our credit scores.

In the same way people strategize about how to win at like, Settlers of Catan or Apples to Apples. There are TRICKS to a credit score, people! And I didn’t know about any of them! Probably because when anyone brought things like “credit bureaus” I immediately found somewhere else to be!!!

How Your Credit Score is Compiled

Get on your tinfoil hats, it’s time to discuss how this super important number is calculated. Important to note is that there are THREE credit bureaus, and they all calculate your score a bit differently.

Is this overwhelming? Heck yes.

Will you likely save thousands of dollars by understanding how to build your score and get lower interest rates on stuff? ALSO yes!

Here are the top 4 contributors to your credit score (with tips on how to leverage these to your advantage!):

Factor #1: Payment History is MOST IMPORTANT

Above all else, your payment history (ie how often you miss a payment) is CRITICAL. I used to miss payments all of the time, especially on my Wells Fargo student loan.

Eeek.

From Equifax: “Credit scoring models generally look at how late your payments were, how much was owed, and how recently and how often you missed a payment.”

GAME THE SYSTEM: Put everything on auto-pay. If funds are tight and you’re worried abut going into overdraft, then set up calendar reminders to check your accounts before your payment goes through. I also make my auto-pay abut 15% above the required payment, just in case there are fees I don’t see.

I’ve set up automatic payments on everything, and on the first of every month I check to make sure they’ve gone through! I’ve had payments get missed because I got a replacement card, sometimes errors happen, etc.

If something happens and. you can’t make a payment, don’t despair and let the bill sit on your counter. CALL the organization, and see what you can work out.

#2: Credit Utilization | Don’t Max Out Your Cards

I *really* wish I had known this in college. “Credit Utilization” is how much you’re using on your card, and should be no more than 30%. We should use no more than 30% of the available credit on a card.

Confused? Been there.

Let’s say you have a credit card with a limit of $10,000. The credit bureaus see responsible spending as having a large portion of that unused. You should have no more than $3,000 out on that card (ideally paying it off monthly!).

30% cap!

Having maxed out (or close to maxed out) cards makes you appear riskier to lenders.

GAME THE SYSTEM: I’m in a tough spot on this one, as I maxed out a credit card to help me get through my last year of college. Womp. This card is at 23% APR Interest (barf), and I recently found out that most of my payments were going to interest, meaning I’d take forever to pay it off.

UGH.

So I lowered my payments on other accounts, to throw as much money at this card as possible. As I do this, my credit score will improve. And I’ll eventually refinance this card at 0% interest (switching the balance to the US Bank Vis Signature Card, so that I can pay off the remaining balance without pesky interest!

A second (but dangerous!) tactic is to open up a new credit card, but only spend like $50 a month on it. This increases your available credit. However, this can be dangerous if you lack self-discipline when online shopping (hi, it me!) or spend money emotionally.

#3: Account Diversity

This one is a little weird, but basically a credit bureau wants you to have different types of credit. We want to avoid ONLY having credit cards on our reports.

Mix up what you got going on!

From Equifax: “Credit score calculations may also consider the different types of credit accounts you have, including revolving debt (such as credit cards) and installment loans (such as mortgages, home equity loans, auto loans, student loans and personal loans).”

GAME THE SYSTEM: This one is a bit tricky, because opening lines of credit for the sake of your score (that you don’t need), is silly. I’m letting my account diversity build up over time.

Some families are able to game the system by having putting a second family member on a car loan, mortgage, credit card, etc. AS the older family member pays on the account, the younger builds up their credit.

#4: Length of Credit History

This relates to #1, in that credit bureaus like to see a longer length of credit history. The earlier one can RESPONSIBLY get and pay on a credit card, the better.

This also means people generally keep their oldest credit card open, even if they just use like $25 a month on it and pay it off. Closing your oldest credit card can have a negative impact on your credit, ugh.

GAME THE SYSTEM: Keep your oldest credit card active – but barely. Buy a few things a month, and pay off the balance immediately.

MY CREDIT FIXING PLAN FOR MOI

Okay, so now that we’re all on the same page about how credit works, I want to share my plan to get to a 750 credit score (and get the Chase Saphire card, which is chock full of rewards):

Tactic #1: Put Everything on Autopay && CHECK TO BE SURE BILLS ARE PAID

Late payments will screw up my score, so I have automatic payments set up for my car loan and insurance, medical bills, credit cards, etc. On the 1st and 15th of the month, I go into my accounts and CHECK TO MAKE SURE THE MONEY HAS BEEN PAID.

Errors happen. But I’m not gonna let those errors impact my credit, dang it!

Tactic #2: Pay 15% Extra on Bills

I like to pay 15% extra (so if a bill is $100, I pay $115), as this extra amount is often applied to next month’s bill. This has gotten me me a grace period if a payment doesn’t go through. The bill shows up as “partially paid” not “delinquent” on some accounts.

Tactic #3: Tackle Biggest Interest Rate First

I’ve lowered my payments on other things (student loans, etc) to tackle my pesky Wells Fargo credit card that’s at 23% APR Interest. I realized I need to just annihilate this card, as I’m paying a crap ton in interest fees!!

Once this card is at half its balance, I’m going to apply to refinance this card through another institution and get 0% APR. Then I’ll be able to put 100% of my payments to the balance, not interest.

I am also using my upcoming Blogger Closet Sale to attack this credit card, and I’ve come up with a new course! The profit from this course will be used to pay off this card.

Tactic #4: Building Credit with Self.Inc

I don’t have a mortgage, and I don’t want to open more cards to get my credit utilization rate down. So, I’ve been using Self.Inc to help build my credit.

The “TLDR” version of this is that I applied for a $500 loan from Self.Inc – but I don’t get the money. It’s put in an account administered by Self, and I make on-time payments to Self on the loan. Self then reports those on-time payments to credit bureaus, building up my “Payment History” section of my credit report.

After I’ve paid the loan off, I get my money back, minus Self fees.

From Clever Girl Finance:

For the in-depth details, you’ll want to visit Self.Inc, here!

Two Types of Financial Bloggers // YOU CAN DO THIS!

Most bloggers who write about personal finance fall into two camps. Either they’ve always been a personal finance nerd, dutifully saving a % of their babysitting money, OR they woke up one day to realize they were NOT where they wanted to be financially. In fact, they’re a little bit of a mess.

I’m definitely Camp #2. I love money and money loves me . I’m so SO good at making money. But the backend management and leveraging of money? Let’s just say that’s been a DIY project of mine.

You Can Do This, Too!

I want to end this blog post with the encouragement that you may feel like you’re TERRIBLE with money, but there are resources at your finger tips to help you make big money moves. I’ll be updating my blog with more on my money journey (gonna write about my retirement plan, getting started investing, etc).

Be sure to join me via email to get updates!

What to read next —>

- How to Make More Money in 2021 | 7 Easy Tips

- How to Raise Your Freelance Rates | Step-By-Step Guide to Make More Money

- Is it worth it to get an Ellevest Coaching Session? | Making Money Blogger

Want More Great Posts Like This?

If you want to stay up-to-date on posts from The Huntswoman, I recommend joining me on your favorite social media platform (Facebook, Instagram or Twitter).

More of an email kind of person? Join my business and career focused email list here, and/or my fashion-focused email list here!